From FOMO to FOOP: why the property wealth narrative is changing

If your parents bought a house and sold it for a small fortune, this is the piece that explains how that worked, and whether the same conditions still exist.

From FOMO to FOOP

There is a saying that circulates quietly among property watchers: you want prices to go down until you own one.

It captures how quickly a buyer's interests flip. The renter watching auction clearance rates with a mix of frustration and calculation becomes, the moment they sign a contract, someone who checks CoreLogic on a Saturday morning hoping the line has gone up.

In 2026, something is shifting. Housing analysts have a name for it: FOOP. Fear Of OverPaying. Where FOMO pushed buyers to act fast before they were priced out, FOOP is the anxiety that you are paying too much into a softening market. By May 2026, prices in Sydney and Melbourne were already falling.

FOMO did not appear from nowhere. It was built from specific conditions. Understanding those conditions, and how they are changing, is what this piece is about.

Where the story came from

The dinner table story, someone's parents or neighbour who bought in a suburb for a fraction of today's price and sold for a multiple of it, was not random. It was real. But it was built on a specific policy architecture, not on a natural law that property values always rise.

The pivotal moment was 1999. The Howard government replaced the existing system of indexing capital gains for inflation with a flat 50 per cent discount for assets held longer than twelve months. From that point, property became one of the most tax-advantaged investment classes available to ordinary Australians.

Economist Saul Eslake spent over twenty years saying what most property commentators would not. Investors buying existing homes, he argued, put "upward pressure on house prices and increases demand for rental housing when they outbid potential first home buyers at auctions." The IMF and OECD flagged Australian housing as overvalued relative to incomes in their annual economic reviews for years running. Both assessments were consistently set aside.

Sydney's median house price was around $260,000 in 1999. By 2024 it was approaching $1.5 million. That trajectory was not purely population growth. It was the 1999 policy change compounding over 25 years, amplified by a decade of historically low interest rates from 2012 to 2022.

The FOMO was not irrational given those conditions. The conditions were the problem.

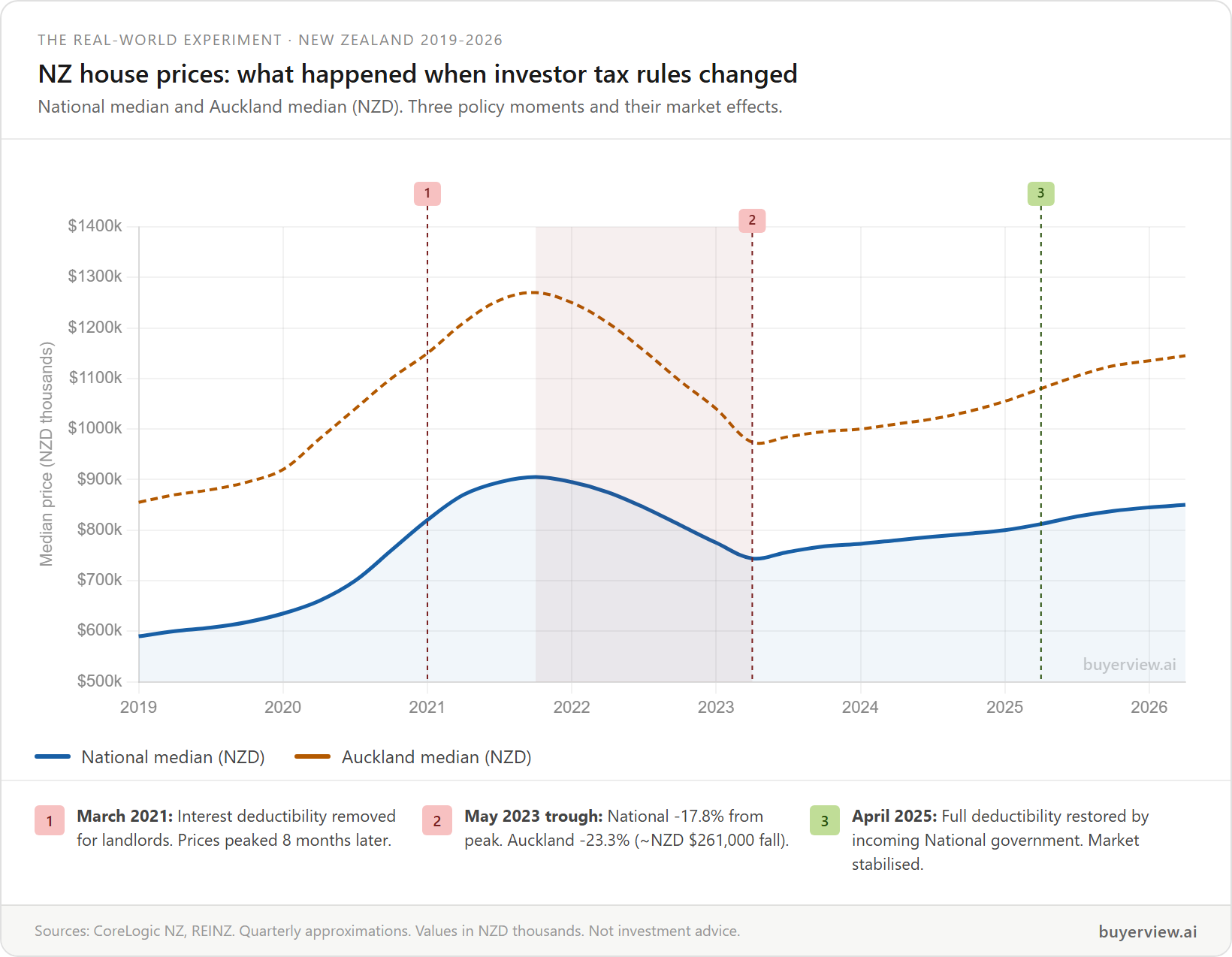

New Zealand ran the experiment first

The closest real-world test of what happens when you remove the investor tax incentive is New Zealand.

In March 2021, the Ardern Labour government removed interest deductibility for residential property investors.

Sources: CoreLogic NZ, REINZ. Values in NZD. Not investment advice.

National house prices fell 17.8 per cent from peak to trough. In Auckland the fall reached 23.3 per cent, a drop of roughly NZD $261,000 on the median. When the incoming National government under Christopher Luxon restored full interest deductibility from April 2025, the market stabilised and prices began recovering.

One lesson from New Zealand: the investor tax incentive was the engine. Remove it and prices fall. Restore it and prices recover. Australia's 2026 budget is not a direct copy of the New Zealand approach. The redesign applies to established properties only and phases in from 1 July 2027. But the mechanism is the same, and New Zealand has already run the experiment.

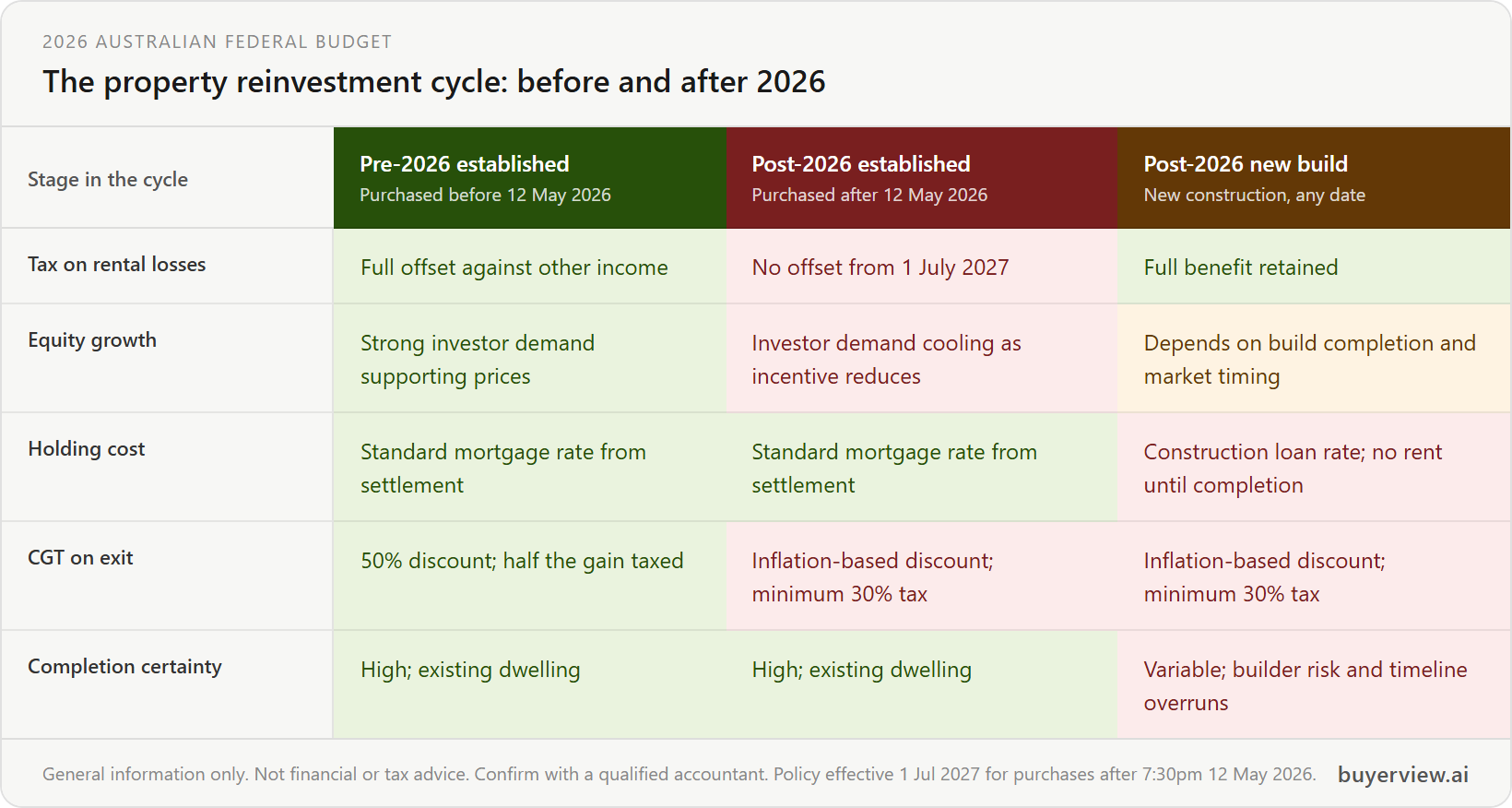

The reinvestment cycle: how it worked, where the friction is now

The 2026 changes only make sense if you understand how property investors actually built wealth. Not just by buying property, but by running a tax-efficient reinvestment cycle.

The pattern: buy an investment property, use negative gearing losses to reduce income tax, let the property grow in value, access the equity without selling, use that equity as a deposit on the next property, repeat. When selling, the 50 per cent CGT discount kept more of the gain in the investor's hands to reinvest. Each step in that cycle was tax-advantaged. The returns were not just price growth. They were price growth amplified at every stage.

The 2026 budget does not dismantle that cycle. It reduces the efficiency at multiple points simultaneously.

For investors in established properties purchased after 12 May 2026, the tax offset on losses is restricted, equity growth may slow as investor demand cools, and the CGT discount is replaced with a reduced inflation-based calculation from 1 July 2027. The compounding still works. The tailwind at each step is weaker.

The new build redirect and what it means for construction

The redesign directs negative gearing toward new builds, pushing investor demand toward new construction rather than competition for existing homes.

But the construction sector that must deliver that supply entered 2026 under strain. A wave of builder insolvencies from 2021 to 2024, Porter Davis among the most visible, was driven by fixed-price contracts colliding with inflation. Trades shortages have not resolved. The government's own 1.2 million homes target is already behind schedule.

Channelling investor demand into this environment risks pushing construction costs higher and timelines longer. For investors, that means loan holding costs during a build that runs over schedule, and a final bank valuation that may not meet expectations. A construction loan sits at a higher rate than a standard mortgage, and it runs for the duration of the build with no rental income to offset it.

First home buyers want new builds too. The First Home Guarantee applies to new builds and established properties. When investor demand concentrates on new construction, first home buyers compete in that same segment. A different market, the same competition.

You own one now

Buyers who purchased between 2022 and early 2026 now sit on the other side of that original saying. They want prices up. But the affordable housing goal and the personal wealth growth goal pull in different directions, and the 2026 budget has chosen one of them. That direction has a documented track record one country over. This is not a reason to panic. It is a reason to buy clearly, not on narrative.

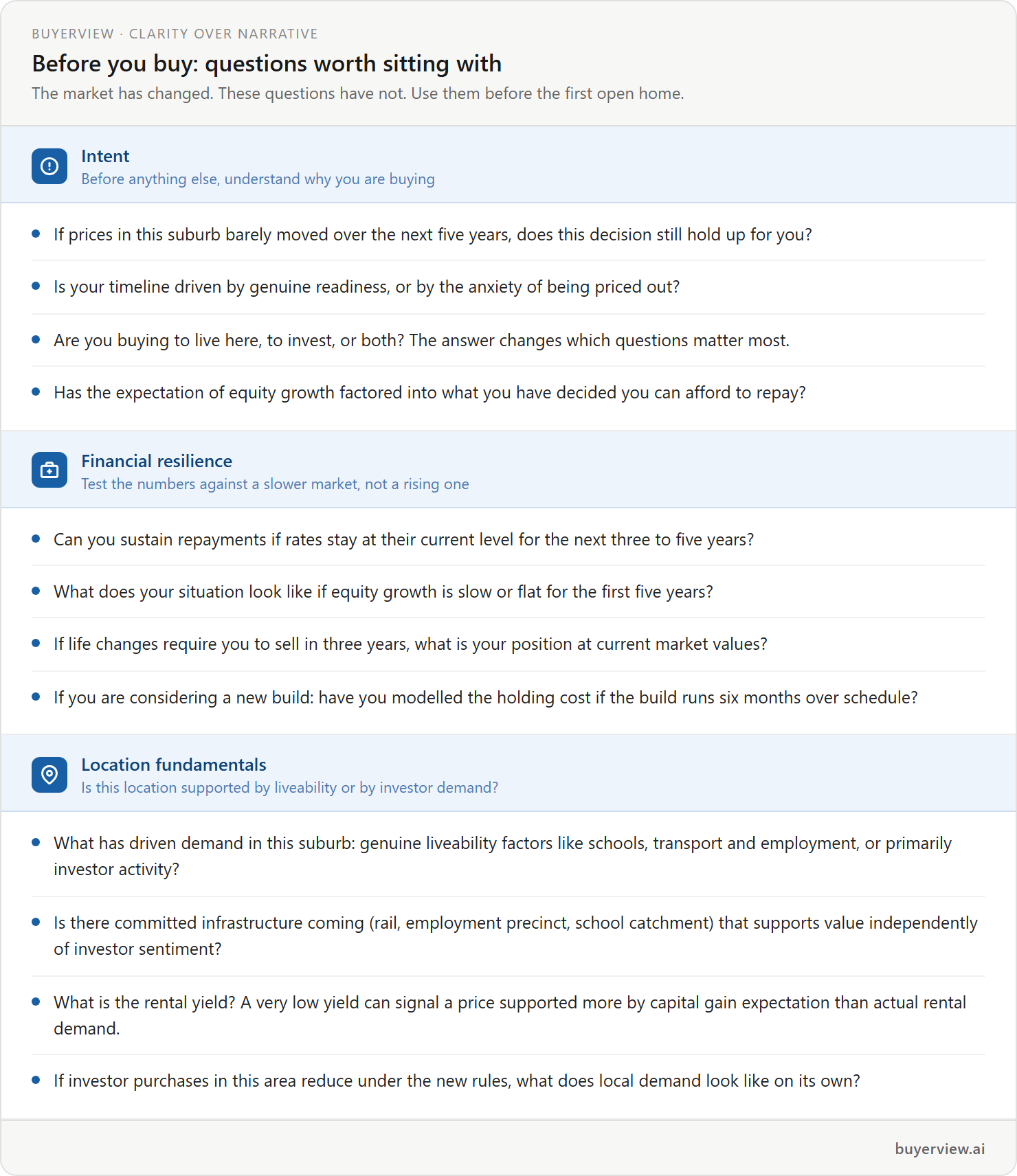

From narrative to clarity: questions worth sitting with

The old property narrative was a blanket: buy anything, wait, the market does the rest. That blanket was woven from specific policy conditions, a low-rate environment, and investor demand that no longer operates the same way for established properties.

The antidote to a blanket narrative is specific questions about a specific property in a specific life situation. FOMO pushed buyers to decide fast. Clarity allows them to decide well.

Some of these questions belong in a conversation with yourself before you walk into a first open home. Others belong at the property, directed at the agent. The questions in the card above do not change with the budget. The market does. Asking them costs nothing.

Frequently asked questions

How has negative gearing changed under the 2026 federal budget?

For established properties purchased after 7:30pm on 12 May 2026, rental losses will no longer offset other income from 1 July 2027. New builds retain the full benefit.

What happened to property prices in New Zealand when similar investor tax changes were introduced?

National prices fell 17.8 per cent peak to trough and Auckland fell 23.3 per cent. When the incoming government restored deductibility in April 2025, prices recovered.

What does limiting negative gearing to new builds mean for construction costs and housing supply?

It channels more investor demand into an already strained construction sector, which risks pushing build costs and timelines higher for both investors and first home buyers competing in the same market.

Disclaimer

General information only. Not financial, tax, or legal advice. Policy details are based on the 2026 federal budget as announced. Confirm your position with a qualified financial adviser or accountant.

BuyerView helps Australian property buyers ask the right questions, on the record, before they buy. Ask your first question free